Faculty of Environmental and Information Sciences

Department of Management and Information Sciences

- Key words

- The information disclosure system, accounting information, environmental information

Doctor of Business Administration / Professor

Mayumi Tanaka

Education

Graduate School of Business Administration , Kobe University (Master’s Program)

Graduate School of Business Administration , Kobe University (Doctoral Program)

Professional Background

Research assistant at the Research Institute for Economics and Business Administration, Kobe University

Part-time lecturer at Kobe Gakuin University

Consultations, Lectures, and Collaborative Research Themes

Corporate financial statements analysis

Comparison of corporate environmental measures based on a qualitative approach

Main research themes and their characteristics

「Consideration about the significance of the segment information disclosure system」

The information disclosure system is established due to the relationship between the information disclosure side (e.g., companies) and the information disclosure request side (e.g., government, investors, local residents, etc.). Although the information disclosed is wideranging, when a company discloses its financial condition and business performance, the information is called accounting information.

Among the accounting information, the business activities of a company are broken down into categories (segments) such as by industry and region, and information about sales and profits by this category is called segment information. It is said that segment information has come to be released as information useful for grasping the actual situation of the company as the internationalization and diversification of the company progresses. Behind this is the existence of investors who strongly demand the securities investment decision support function that accounting information should provide information that contributes to investors' decision making.

However, the timing of the internationalization and diversification of companies and the timing of the appearance of investors as mentioned above are very different between the United States and Japan. Therefore, the significance of the information disclosure system was examined through a literature survey. As a result, it was found that the problem behavior of companies became prominent at the same time as above. The role of the government at that time was the information disclosure request in order to control the problem behavior of companies.

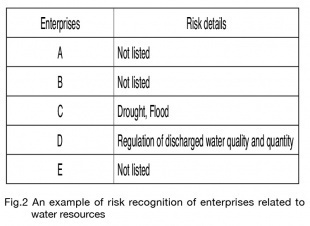

「A study on corporate risk awareness of water resources-related disasters」

In recent years, the frequency of disasters related to water resources has increased, and the damage amount has also increased. Particularly in the case of companies, there is a possibility that tangible fixed assets such as buildings and machinery will be damaged, resulting in a large decrease in asset value and productivity, and disruption of the supply chain. If this happens, it will not only be difficult for the company to continue its own business activities, but it may also lead to disruption and stagnation in the market economy.

Companies are working on environmental measures to prevent the above damages. Information on these efforts has been disclosed in the environmental reports issued by the companies themselves, but the scope of disclosure is extremely limited.

Therefore, the Ministry of the Environment has launched a new " ESG dialogue platform" so that the efforts of companies can be viewed on the library as environmental information. The difference between the data on the ESG dialogue platform and the data on the environmental report is that the companies themselves identify the important environmental issue areas, and also the "corporate strategy", "risk", and "opportunity" in that area. In order for a company 's efforts to be carried out effectively, it is essential to recognize the environmental issues that companies face and the risk awareness of those environmental issues.

At present, it was found that the number of companies that recognized disasters related to water resources as a risk was limited to a very small number of companies.

Major academic publications

Mayumi Tanaka, Hidetoshi Yamaji, US segment accounting system theory –By focusing on accounting standards of military-Industrial complex companies- , the Research Institute for Economics and Business Administration, Kobe University, 2017.

Mayumi Tanaka, “Draft proposal on water risk assessment by enterprises -By using information on ESG dialogue platform- ”, Sustainable Management No.19, 2019, pp.88-101.